It is laborious to argue with the sorts of outcomes Eli Lilly(NYSE: LLY) has produced over the previous 5 years. The corporate has been one of many best-performing pharmaceutical giants, with its shares leaving the broader market within the mud.

Some may argue that it is too late for traders to get in on Eli Lilly, whereas others might really feel that its work within the diabetes and weight problems markets nonetheless makes it a beautiful long-term choice. Which aspect is true? Let’s work out how Lilly might carry out by the tip of the last decade, and determine whether or not it is nonetheless price investing within the inventory.

First, let’s take into account how Eli Lilly’s latest merchandise will have an effect on its efficiency within the subsequent half-decade. These new medicines embrace Alzheimer’s illness remedy Kisunla, ulcerative colitis remedy Omvoh, and most cancers drug Jaypirca.

In fact, Lilly’s most vital new merchandise are diabetes remedy Mounjaro and weight administration drugs Zepbound, which share the energetic ingredient tirzepatide. In 2024, Eli Lilly’s income elevated by 32% yr over yr to $45 billion. The tirzepatide franchise contributed about $16.5 billion — regardless of having been available on the market for lower than three years.

Analysts have predicted peak annual gross sales of $25 billion for this compound. They could have been lowballing it. I count on Zepbound and Mounjaro to proceed on their upward trajectory by 2030, though elevated competitors will in all probability result in their delivering much less spectacular gross sales progress.

Nonetheless, the opposite medicines in Lilly’s new portfolio, which are not but contributing a lot, will rise in prominence. Think about Kisunla, which fills a big want in treating Alzheimer’s illness. In accordance with some estimates, it might generate about $2.5 billion in income by 2030. Jaypirca and Omvoh must also contribute meaningfully by the tip of the last decade.

In different phrases, Eli Lilly’s income ought to proceed rising at a great clip. The midpoint of the corporate’s steerage for 2025 implies gross sales progress of about 32% for the yr, a terrific efficiency for a pharmaceutical large. I might be stunned if its annual top-line progress goes decrease than 15% in any yr by 2030.

Eli Lilly has a number of thrilling merchandise in its pipeline, a few of that are more likely to earn approval within the subsequent 5 years. Think about two of the corporate’s main candidates in weight reduction: orforglipron and retatrutide. Each medicines are in section 3 research, however not simply as weight reduction administration merchandise: They’re being developed as potential therapies for diabetes, sleep apnea, and a number of other different circumstances.

What makes them so promising? Think about retatrutide, a triple agonist — it mimics the motion of three hormones: GLP-1, GIP, and GCG. That could possibly be an enchancment on even tirzepatide, which mimics GLP-1 and GIP. Tirzepatide was the primary of its variety. Retatrutide nonetheless has to show its price in scientific trials.

The purpose is that Lilly’s pipeline within the more and more aggressive GLP-1 market appears stronger than that of any of its friends not named Novo Nordisk. In accordance with some estimates, retatrutide might generate $5 billion by 2030, whereas orforglipron may attain $8.3 billion in gross sales by then.

Naturally, different new Lilly merchandise might see the sunshine of day by 2030, and others will progress to late-stage research. That could possibly be the case for the drugmaker’s extremely promising investigational gene remedy for deafness. Moreover, lots of its current merchandise will seemingly earn label expansions. The lineup ought to look even stronger by the tip of the last decade.

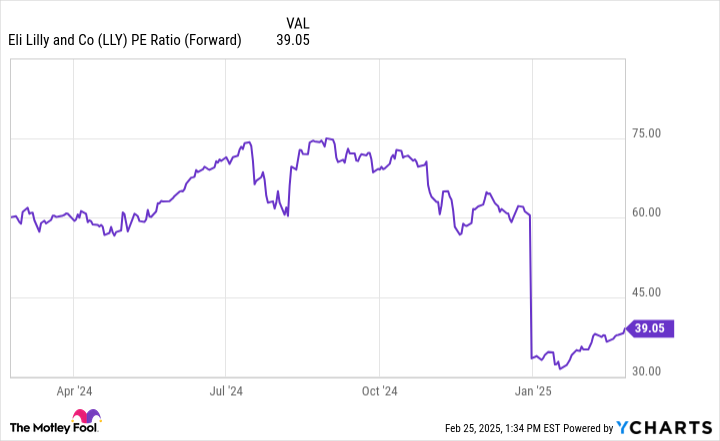

Bears may level out Eli Lilly’s ahead price-to-earnings (P/E) of 39.

The healthcare business’s common is 17.7 as of this writing. If Lilly is overvalued proper now, it would underperform broader equities within the medium time period. Would it not be greatest for traders to attend for a greater entry level?

My view is that the inventory is pretty valued. Lilly’s income and earnings have been rising a lot sooner than these of most of its equally sized friends within the healthcare business, so it solely is smart that it has a better ahead P/E.

I count on Eli Lilly to beat the market by the following 5 years. Past that, contemplating its unimaginable revolutionary talents, it’ll nonetheless be a superb inventory.

Before you purchase inventory in Eli Lilly, take into account this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they imagine are the 10 greatest shares for traders to purchase now… and Eli Lilly wasn’t one among them. The ten shares that made the minimize might produce monster returns within the coming years.

Think about when Nvidia made this record on April 15, 2005… in case you invested $1,000 on the time of our suggestion, you’d have $765,576!*

Now, it’s price notingInventory Advisor’s whole common return is890% — a market-crushing outperformance in comparison with173%for the S&P 500. Don’t miss out on the most recent high 10 record, accessible whenever you be a part ofInventory Advisor.

{kind=link}